What Is the Debt Snowball?

If you are struggling with debt, the good news is that there are strategies you can use to pay it off. The debt snowball method is a simple approach where you start by focusing on your smallest balance first. With each debt you pay down, you’ll move on to tackle a larger debt until you are debt-free.

Here is everything you need to know about successfully paying off your debt using the debt snowball method.

What Is the Debt Snowball?

The debt snowball method involves tackling your smallest debt first. While making the minimum payments on all your debts, you’ll funnel any extra money you have available towards your smallest debt. This will help you pay it off faster.

Once you’ve reached the milestone of paying down your smallest debt, you can move on to your next largest debt. Since you’ll have one less minimum payment to make each month, you can use that savings to pay off your next largest debt more quickly. You then repeat this process until all your debts are repaid.

Not only will the financial impact of the debt snowball grow as you eliminate your monthly payments one at a time, but the feeling of achievement that comes with erasing each debt will increase as well. As you eliminate each of your debts, you will see your progress and maintain the motivation needed to keep moving forward.

Related: How to Apply Extra Money to Your Debt Payoff Plan (Using the Undebt.it Tool)

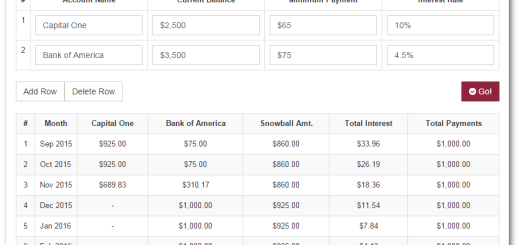

The Debt Snowball: An Example

Let’s say you have three debts:

- $10,000 auto loan

- $3,000 credit card balance

- $1,000 medical bill

With the debt snowball strategy, you pay the monthly minimum on each of your debts. You also try to make extra payments on your medical bill so you can eliminate the minimum monthly payment for that debt entirely. If your medical bill requires a minimum payment of $50 per month and you are able to pay it off completely, that means you’ll have an extra $50 each month to put towards your credit card debt. This will allow you to repay your credit card balance more quickly.

The snowball will grow again when you eliminate your credit card balance. At that point, you’ll be able to put the minimum payments from your medical bill and credit card debt in addition to any extra money you have towards your auto loan. With a larger snowball, you’ll be able to pay off your auto loan faster.

What Are the Pros and Cons of the Debt Snowball?

As with all financial strategies, you should be aware of the pros and cons.

What Are the Pros of the Debt Snowball?

Paying off debt requires strong internal motivation since it can be a lengthy process. As a result, it can be hard to stay dedicated to your repayment goals. The primary benefit of the debt snowball is that you’ll be able to enjoy small wins that will keep you going along the way.

As you move through the debt snowball process, you’ll erase your small debts quickly. These initial wins can give you the motivation you need to keep going. Without little victories throughout the journey, it can be a challenge to stick to your goal of becoming debt-free.

Additionally, this is a tried and true debt repayment strategy that has helped many people eliminate their debts. If you can stick to the debt snowball method, you’ll walk away from the process completely debt-free.

What Are the Cons of the Debt Snowball?

One flaw in the debt snowball method is that you could be missing out on an opportunity to save money on interest payments. This is because the debt snowball strategy focuses on loan size, not interest rates.

If you have larger loans with higher interest rates than your smaller loans, you will pay more in interest charges. Depending on your loans, this could cost you a significant amount of money.

Related: New Hybrid Payoff Method: Debt-to-Interest Ratio

Why Does the Debt Snowball Work?

The debt snowball is an effective debt repayment strategy because of the way our minds work.

In a study published in the Journal of Marketing, researchers found that people tend to break down large projects into more manageable tasks. With small actionable steps, most people are more likely to make lasting progress towards a goal.

The same holds true for debt repayment. When you look at your total debts, it can be overwhelming to consider repaying it all without breaking down your goal into individual debts. Deciding to pay off the smallest debt first allows you to start your journey with one manageable action step.

This repayment method lets you have small wins throughout your debt repayment journey. Each time you eliminate a small debt, you will enjoy the accomplishment of wiping one of your debts off the books. That psychological win can give you the boost of mental fortitude required to keep moving forward.

You could save money by working on a debt repayment strategy that minimizes the total interest paid. Keep in mind that you might run into the issue of maintaining momentum if you give up these smaller wins for savings. Ultimately, this could cost you even more money in the long run.

Each small success reminds you of why you are pursuing a debt-free life and motivates you to move forward.

Is the Debt Snowball Right for You?

The debt snowball is a good option for anyone who knows they will be motivated by small successes during their debt payoff journey.

If you think you will struggle to stay motivated, then the debt snowball is the perfect way to safeguard against losing steam. Each little victory will propel you towards your end goal of becoming debt-free.

I’ve created a free debt snowball calculator that allows you to test out several methods of debt repayment, track your progress, and see how “snowflakes” can help you get out of debt even faster. Explore your debt repayment options today and take the first step towards eliminating your debt for good.